The British love affair with rental property combined with the new pension freedoms is a potentially dangerous combination. A recent report entitled “The Runway to Retirement”, published by Engage Insight, suggests that as many as 30% of retirees could invest their pension fund in property, in one form or another.

Buy-to let is likely to be the most popular option and as ever, the people most at risk are those not seeking advice. Estate agents are already being approached directly by clueless first-time landlords, buying up low value property in poor rental areas. Having committed to the property, some will find that their rental yield falls well short of their expectations.

Taxation and Costs

The potential taxation to access the pension fund and associated costs will have a significant impact on the value of the property that can be purchased. Most members of the public think Pensions Freedom means they are free to take their pensions. They are, but few will be happy to pay large amounts of tax to do so.

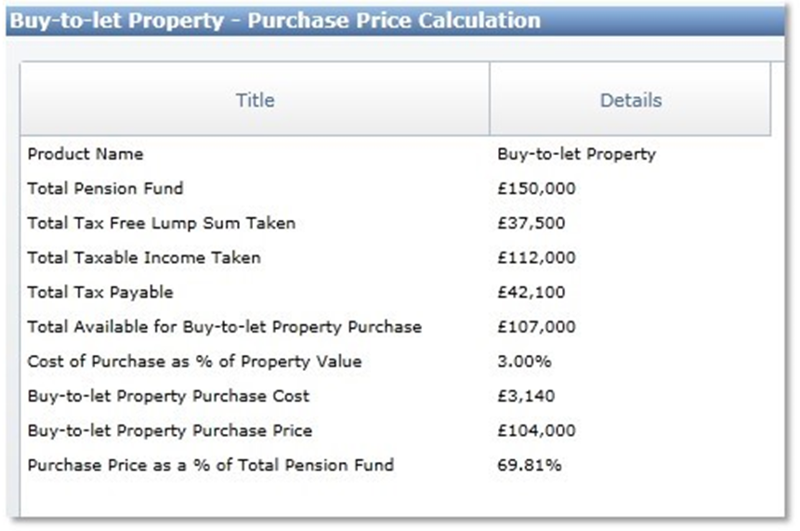

As rental yields are linked to property values, the returns could be around 1/3rd lower than first envisaged. The table to the right shows how a pension fund of £150,000 might buy a property worth only £104,000. Some assumptions have been made, but there arguably should also be an emergency fund for repairs within the rental property. After all, when the boiler breaks down, the tenants expect it to be fixed quickly!

Decumulation vs Accumulation

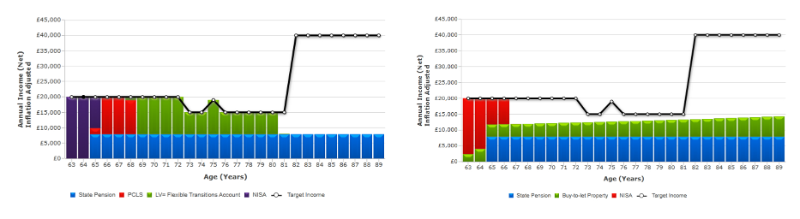

At a time when you could be decumulating your retirement pot in a drawdown plan, these landlords will find themselves accumulating within a single asset in the property sector. The charts below illustrate this concept clearly.

- The decumulation within Flexible Access Drawdown and ISA gradually reduce funds from £200,000 at age 63 down to zero at age 80. At this point, the client is reliant on the state pension.

- Under Buy-To-Let, there is an immediate pension fund drop from £150,000 to purchase a property for just £104,000. From this point, its value might grow steadily throughout retirement. When viewed together, the decumulation vs accumulation concept is quick and easy to demonstrate to prospective landlords.

- No allowance has been made for Month 1 taxation here. If any excess tax is collected, it needs to be reclaimed by someone who probably doesn’t ordinarily submit tax returns. As a result, the property purchase and therefore, the income stream could be delayed.

Target Income

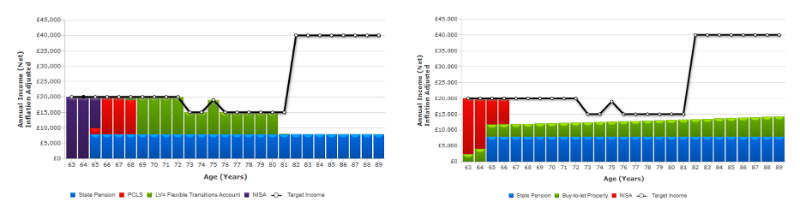

Having already mentioned that rental yields will be linked to the value of the property, it’s time to look at income. The charts below both target a net annual income of £15,000, with a £5,000 increase in the early retirement years to fund travel. At age 75, there is a one-off requirement for a Silver Wedding party and care home fees have been assumed from 82.

- The flexible access drawdown delivers the required target income from the ISA for the first three years. From 65, the client is living on a combination of State pension and PCLS, with the drawdown income being paid until age 80. From 80, all pots are exhausted, leaving state benefits as the sole income source.

- The buy-to-let fails to deliver the required level of target income once the ISA is exhausted at age 66. You’ll set your assumptions, but an upwards only property value increase combined with 2.5% inflation (illustrated here), is far from guaranteed.

It’s easy to go to town and consider the capital gains situation if the property needs to be sold or perhaps the possible inheritance upon death. However, this additional analysis shouldn’t be needed if clients can understand what a bad idea buy-to-let might be for perhaps their biggest asset.

Data courtesy O&M Systems