What will it take – to get everyone believing?

The climate crisis is “wreaking havoc” on the planet’s water cycle, with ferocious floods and crippling droughts affecting billions of people, a report has found.

Water is people’s most vital natural resource but global heating is changing the way water moves around the Earth. The analysis of water disasters in 2024, which was the hottest year on record, found they had killed at least 8,700 people, driven 40 million from their homes and caused economic damage of more than $550bn (£445bn).

Rising temperatures, caused by continued burning of fossil fuels, disrupt the water cycle in multiple ways. Warmer air can hold more water vapour, leading to more intense downpours. Warmer seas provide more energy to hurricanes and typhoons, supercharging their destructive power. Global heating can also increase drought by causing more evaporation from soil, as well as shifting rainfall patterns.

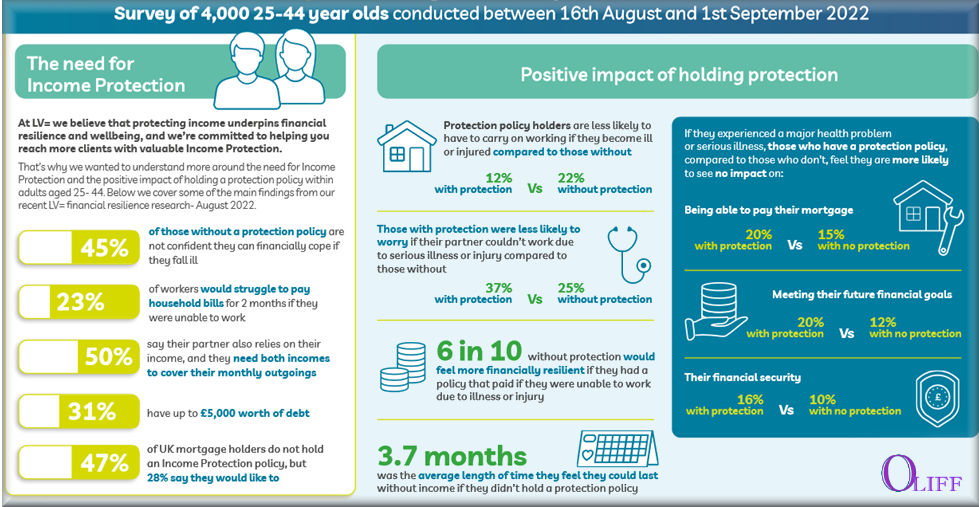

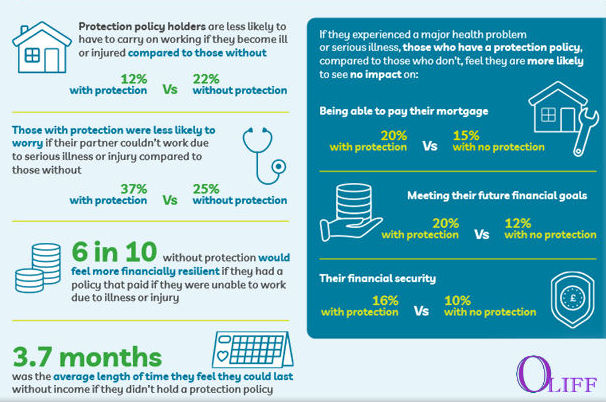

For clients who need to think about putting themselves or their immediate

family into care, it can be a daunting, emotional and stressful time.

A huge part of this stress can be down to working out how to pay for the care itself.

Unfortunately, care homes haven’t been immune to the effects of the cost of

living crisis. The average weekly cost of living in a residential care home is

£760; for a nursing home it’s £9601. These costs vary depending on where

they are in the UK.

But the UK Care Guide’s 2022 survey found average fees have risen by 11%

between February 2022 and February 2023, with some homes increasing

their individual costs by as much as 30%.

This is down to things like raising staffing costs to attract and retain care workers, rising energy costs to keep homes warm and comfortable, and pricier food bills in the supply chain.

The number of people going into care is increasing significantly, too.

According to the 2022 Office of National Statistics report, 375,035 people

went into care between March 2022 to February 2023 – a 3.1% increase on

the year before.

With the need for professional care increasing due to an ageing population2,

spiralling costs at an already financially pressured time will create more worry

for your clients who are looking at care options for themselves or their

loved ones

Funding for care

The care system in the UK can feel complicated.

With thousands of homes to choose from, it can be hard to know where to start and how to pay for it.

For those who aren’t solely self-funding their care, help is available.

Here are some examples:

It can be difficult navigating this aspect of later life for you or loved ones.

So we can tap into the Legal & General Care Concierge service for when the need arises.

You (or anyone in your immediate family) can call care experts to get more information about finding and funding care. These experts can help

understand all the funding options available such as NHS, local authority,

self-funding and gifting.

Having someone at the end of the phone who knows the system inside-out

can make a stressful time a little smoother.

The world’s green energy transition, which is essential to achieving net-zero emissions and halting climate change, is under threat, as a financial era of rising interest rates has made some projects, like new offshore wind farms, unaffordable.

Estimates suggest that Europe must now find an additional €163 billion to reach net-zero by 2050, with figures likely to be similar elsewhere in the world. As such, firms are pulling back from new projects.

Last week, Swedish energy firm Vattenfall announced it would stop work on an offshore wind farm in the UK’s North Sea, warning development costs for the Norfolk Boreas scheme had increased by 40 per cent due to rising interest rates and supply chain costs.

Rising interest rates have made the green energy transition more expensive.

Measure, plan and make carbon reductions across your organisation

Are you measuring your organisation’s greenhouse gas emissions yet? We’re here to help if you’re ready to start.

Sustainability strategy

Company behind Devon venture hopes it will become a blueprint for projects owned by consumers

A solar power plant.

A ‘shared’ solar park is an option for households who cannot afford solar panels

or who do not own their home. Photograph: Fuyu Liu/Shutterstock

If you would love to have solar panels but don’t own your home or can’t afford the outlay, how about investing in Britain’s first “shared” solar park that is promising cheaper, zero-carbon electricity, direct to your energy bills for the next 40 years?

With two successful community energy schemes already behind it, Ripple Energy is looking for investors for its third: the construction of a 42MW solar park in Derril Water in Devon, not far from the Cornish town of Bude.

Once up and running in the summer of 2024, the project, which is being built by one of the world’s largest independent renewable energy companies, RES, will produce enough electricity to power 14,000 homes across Britain.

Group says forcing polluters to store carbon dioxide underground is needed to help world reach net zero

Fossil fuel companies should be forced to “take back” the carbon dioxide emitted from their products, handing them direct responsibility for cleaning up the climate, a group of scientists has argued.

The principle that the producer of pollution should pay for its clean-up is established around the world, but has never been applied to the climate crisis.

Data provided by LV

This firm is committed to advising clients on better outcomes for the planet. As an example, 20% of funds that we advise on are alternative energy investments.

Our clients, with millions invested in clean energy, are making a real contribution.

Some other funds we support:

– Developing better engineering solutions, such as medical devices and prosthetic limbs.

– Technology that saves energy by stopping the cold escaping from freezer cabinets in supermarkets. Software solutions to manage risk.

– Financing childcare facilities, GP practices ambulances and better care homes.

Britain claims to be at the forefront of the fight against climate change and our scientists and engineers are trusted to provide solutions; your savings and pension pots can make a difference for your children and grandchildren.

Alternative Energy – facts.

The sector offers a range of funds to either provide capital growth, by investing in new developments, windfarms, solar, hydro, anaerobic digestion. Or income generated by buying into long term income contracts, usually 30 years.

Examples of Alternate Energy investments;

One provides money to build has returned 84.17% since its launch in June 2019

The other is an income fund gaining profit from long term energy contracts and returned 101,92% since December 2017.

NOTE: These are no guarantee of future returns

Coal and gas generation is increasing in cost

whilst solar is substantially cheaper.

The economic argument for solar is strong.

For our economies, we want more people to spend on UK holidays – including Wales?

So why . . . https://www.bbc.co.uk/news/uk-wales-62956842

By Brendon Williams BBC News

Visitors booking stays in Wales could face a tourism tax, including those who already live in Wales, the Welsh government has said.

Green home upgrades could also create 140,000 new jobs by 2030, analysis by Cambridge Econometric finds

Insulating homes in Britain and installing heat pumps could benefit the economy by £7bn a year and create 140,000 new jobs by 2030, research has found.

But the uptake of these energy-saving measures depends heavily on government policy, according to analysis by Cambridge Econometrics, commissioned by Greenpeace.

Read more … https://www.theguardian.com/environment/2022/sep/20/energy-saving-measures-could-boost-uk-economy-by-7bn-a-year-study-says

António Guterres said money raised should be diverted to vulnerable nations suffering losses caused by climate crisis

Countries should impose windfall taxes on fossil fuel companies and divert the money to vulnerable nations suffering worsening losses from the climate crisis, the United Nations secretary general has urged.

António Guterres said that “polluters must pay” for the escalating damage caused by heatwaves, floods, drought and other climate impacts, and demanded that it was “high time to put fossil fuel producers, investors and enablers on notice”.

Read more . . https://www.theguardian.com/world/2022/sep/20/un-secretary-general-tax-fossil-fuel-companies-climate-crisis

In a huge industrial shed on Leckford Estate, a farm owned by the supermarket Waitrose in a beautiful part of southern England, a revolution is stirring in the world of mushroom growing. UK production of this crop relies on peat, the incredibly carbon-rich organic matter found in bogs and fens across the country. Peatland contains so much carbon, it is sometimes described as “the UK’s rainforests”.

That is why the UK government has promised to restore 280,000 hectares of peatland in England alone by 2050, to help meet its climate change goals.

When new energy security strategies for Europe arrive, it is essential that they align with climate change goals. False solutions abound, such as kick-starting a UK fracking industry, even though that has already been tried without success.

Thankfully, the answers are already clear. Wind and solar power should be turbocharged, and ideological barriers such as vetoes for onshore turbines in England must be lifted. More electricity links are required between countries, like the UK-Denmark one due to be finished next year. Energy efficiency needs serious government support, and electrification of cars and heating must be accelerated. And, yes, some mix of nuclear power, more energy storage or carbon-capture power stations will be required to support renewables when the sun isn’t shining.

Individuals can’t solve the climate or energy crises on their own, but there are things homeowners can do to help. People on lower incomes need support to cope with high energy prices. But for those able to pay, there has never been a better time to “repair” that roof, with proper insulation and solar panels. Winter is sooner than you think. Let’s seize the opportunity to make sure we weather it.